My thoughts on the liquidation value of Cyteir Therapeutics

Liquidation announced; further upside could be on offer.

On Friday, Cyteir Therapeutics announced it was discontinuing development of its drug candidate CYT-0851 and liquidating to return cash to shareholders. This has been a home run for me since I wrote it up in March. Clearly a liquidation is a great result for shareholders, and Cyteir’s board of directors should be congratulated. It is unusual for a biotech company with so much cash to simply shut up shop and send the money back to shareholders.

The stock closed at 2.60, up 35%. Cyteir was already a large position for me, but I bought more stock on Friday after the announcement around $2.40-$2.50.

I’m writing this post to provide an update on my thoughts on Cyteir’s liquidation value. Full disclaimer: I am not an expert at analysing liquidations, so please do your own work and don’t rely on my numbers. I’ve tried to be conservative, however there can be unforeseen costs and delays when companies are winding down. I should also mention that I don’t see any risk in the vote being approved. Cyteir’s register contains a lot of pre-IPO investors who will be keen to see their cash returned, and there will also be special situation investors buying the stock now the liquidation is announced.

Before we go on, I suggest reading Cyteir’s press release in full.

The key information is below:

Due to the planned discontinuation of CYT-0851 development, and the previously announced discontinuation of Cyteir’s discovery pipeline, the Company’s Board of Directors intends to approve a Plan of Liquidation and Dissolution (“Plan of Dissolution”) that would, subject to shareholder approval, include the distribution of remaining cash to shareholders following an orderly wind down of the Company’s operations, including the proceeds, if any, from the sale of its assets. Prior to winding down operations, the Company intends to complete regulatory and patient obligations from the ongoing clinical trial. The Company will engage independent advisors, who are experienced in the dissolution and liquidation of companies, to assist in the Company’s dissolution and liquidation. The Company also intends to call a special meeting of its shareholders in the second half of 2023 to seek approval of the Plan of Dissolution and will file proxy materials relating to the special meeting with the Securities and Exchange Commission (the “SEC”). If the Company’s shareholders approve the Plan of Dissolution, the Company would then file a certificate of dissolution, delist its shares of common stock from The Nasdaq Global Select Market, satisfy or resolve its remaining liabilities, obligations and costs associated with the dissolution and liquidation, make reasonable provisions for unknown claims and liabilities, attempt to convert all of its remaining assets into cash or cash equivalents, including through a potential sale of CYT-0851, and return remaining cash to its shareholders. The Company will provide an estimate of any such amount that may be distributed to shareholders in the proxy materials to be filed with the SEC. However, the amount of cash actually distributable to shareholders may vary substantially from any estimate provided by the Company based on a number of factors.

As is customary in these situations, the proxy will have an estimate of liquidation proceeds. Until then, we have to make our best guess.

My thinking around liquidation value of CYT

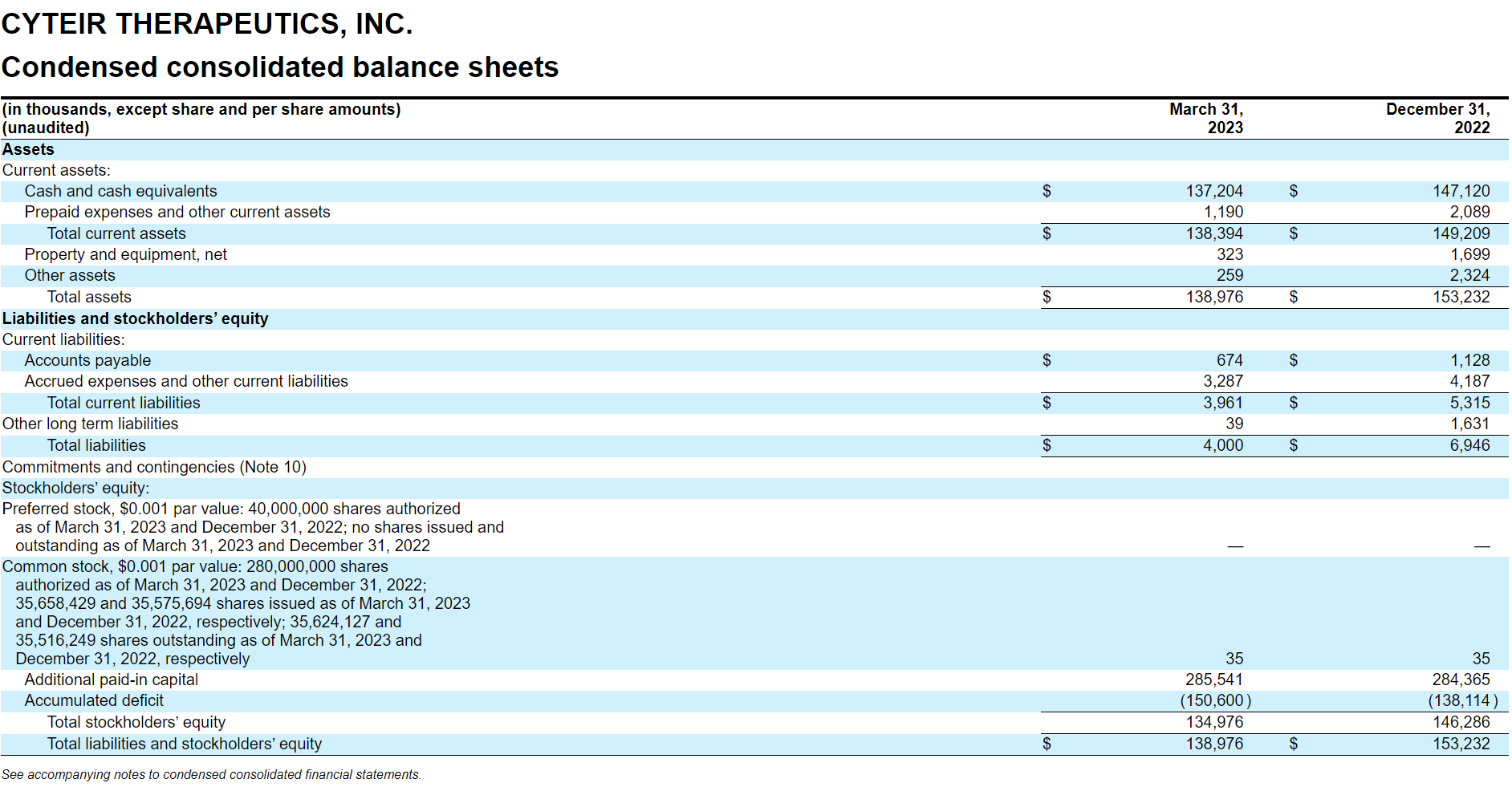

Cyteir reported its results for Q1 in May. On May 4, there were 35,512,837 shares outstanding and 1,049,356 options with a weighted average exercise price of $1.69, which I have included in my diluted share count. At $2.60, Cyteir’s market cap is therefore about $95MM.

Cyteir had a very clean balance sheet at the end of Q1, with $137.2MM of cash, $1.77MM of other assets, and $4MM of liabilities. Shareholders equity at March 31 was $135MM. Cyteir sold most of its PP&E in Q1, and the company’s office lease terminates in October 31, 2023.

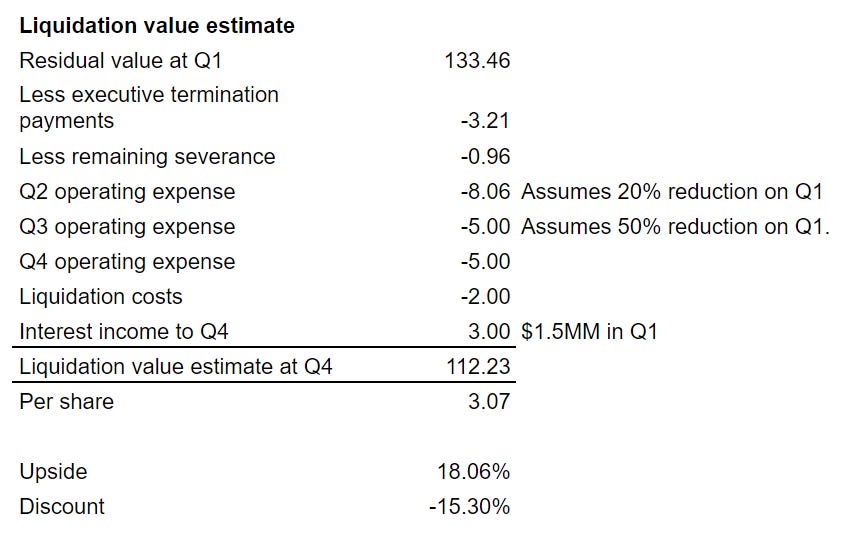

If we take the cash, add the lease security deposit ($259K restricted cash in other assets) and assume zero value for other assets and PP&E, we’re left with $137.46MM of assets. Subtract $4MM for liabilities, and we have $133.46MM in residual value before any further expenses and liquidation costs.

In Q1, Cyteir’s operation expenses were $13.4MM, however this includes a one-off restructuring charge and stock-based compensation, which is not a cash charge. When these items are removed, the adjusted operating expense is $10.08MM.

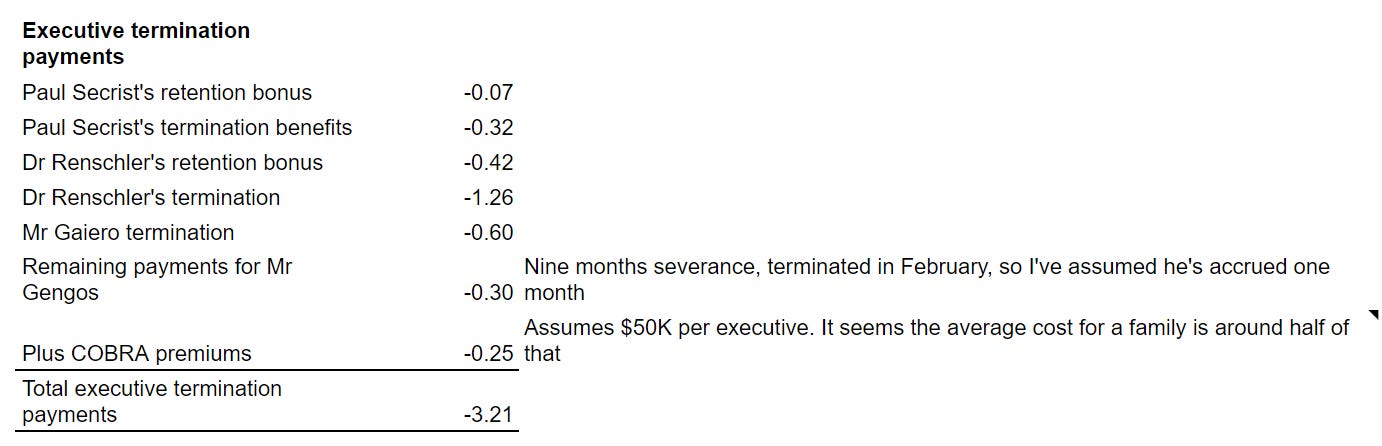

Cyteir had 15 employees in January 2023, following its headcount reduction. Since then, the general counsel, Adam Veness, has resigned. I am assuming roughly $3.2MM in executive termination payments and a further $960K for termination charges for the remaining employees ($80K for 12 employees).

I expect Q2 operating expenses to be lower than Q1, as the workforce reduction wasn’t announced until January 12. Thus, I have factored in a 20% reduction in operating expense in Q2. In Q3 and Q4, I have assumed $5MM of operating expenses. Cyteir has said it will continue providing treatment to patients prior to the liquidation, but I imagine most employees will be let go soon. CYT has also said it would appoint advisors to manage the liquidation. Considering the relatively simple balance sheet, I imagine they will be able to reduce costs significantly. On top of that, I have factored in $2MM for liquidation-related expenses, such as legal fees, etc and $3MM for interest until the end of Q4.

Putting that all together, I get a value of $112.2MM, or $3.07 per share.

Again, I am no expert on liquidations: this is simply my best guess at this point. I could be well off the mark. I have also not factored in a contingency reserve, which is held back during the liquidation process. However, considering CYT’s minimal liabilities and short operating history, I can’t imagine the need for a significant reserve.

Assuming my number here are right, there could be further upside in the event Cyteir sells CYT-0851. I don’t want to count on that, however the press release hints that the company anticipates selling “certain assets”. These certain assets could of course be PP&E, but they could also refer to CYT-0851.

The Company currently expects that its existing capital resources together with the anticipated net proceeds from the sale of certain assets will enable it to meet its remaining liabilities and obligations with sufficient reserves.

As always, I’m keen to hear where I might be wrong here. Let me know in the comments if you think I’m off the mark.

Good write-up and math makes sense at a high level. Any thoughts around the timeframe to finalize the filings for wind-up (in other countries markets you typically need to wait to file final taxes prior to liquidation) - any perspective on this would be appreciated.

I am a 21 year old studying finance in college and was wondering how you go about finding undervalued companies? Is there a specific resource you use to find undervalued companies? And also any books you recommend for doing financial analysis/management?