March portfolio update

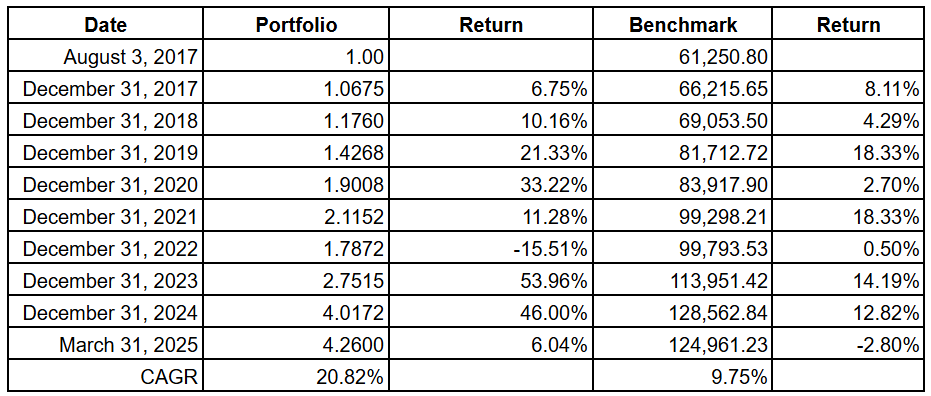

For the three months to March 31, 2025, my taxable portfolio gained 6.04%, while my SMSF gained 3.46%. This is a good result considering that markets generally performed poorly in Q1. My long-term benchmark is the S&P/ASX 200 Franking Credit Adjusted Annual Total Return Index (Tax-Exempt), which is down 2.8% year to date.

The table below shows the returns of my portfolio since inception in August 2017.

My luck continued in early 2025. I had some positions work out nicely, such as CRGX, a short-term busted biotech trade. I bought CRGX in late January after the company announced it was discontinuing a Phase 2 program and reducing its workforce while evaluating strategic options. I was able to buy CRGX as low as $3, which was the intraday bottom. At those prices, I felt CRGX was attractive enough to warrant a large position. I trimmed the stock shortly afterwards at around $3.60 and sold my position at $4. CRGX has since announced a further 80% reduction in force and appears headed for a reverse merger. It currently trades at $4.07, which still seems interesting. However, reverse mergers have a binary outcome. Biotech seems to be particularly troubled at the moment due to changes in the US administration and the FDA. I'm not sure if this will have any impact on reverse merger activity and the market's response.

In less positive news, I made some mistakes which cost me money. For one, I decided to hold on to IKNA after the reverse merger was announced, which hasn't turned out to be a wise decision. The stock is currently down about 22.4% year to date. I also panic sold my Achilles Therapeutics stock at $1.01 in late December. This happened after reading an update from the company with the headline "conclusion of strategic review." Despite positive news in the announcement (the sale of data and assets to AstraZeneca for $12MM), I misread the filing. I assumed the company had finished its strategic process and could continue development or buy another early-stage biotech program. Almost immediately, I realised I was wrong. I bought back my stake at $1.14, but not as much as I sold. Shortly after all of this, ACHL announced it would liquidate and the stock rose to around $1.40. I've since sold my stake at $1.41.

In other bad news, Merchant House International (MHI.AX) announced that it had sold its equipment at a deep discount to book value. While I considered this a possibility, I was expecting a better outcome. MHI is currently halted due to a lack of an Australian director. It still needs to sell its US property before it winds up. It seems likely that I will lose money on the position. It's unclear how long the wind-up process will take. I should have been more careful considering the type of assets involved in the liquidation.

Outside of the busted biotechs, my Japanese positions performed strongly in the three months to the end of March. I have three positions in Japan, which collectively make up 40.2% of the portfolio: CEL Corp (5078.T), Mitachi (3321.T) and another company which I haven't disclosed as yet. Overall, I'm very comfortable with these positions, even though they are more expensive lately.

Mitachi has not risen as much as some of its peers, and appears compelling at current prices. At 1,170 yen, Mitachi has a market cap of 9.3B yen and an enterprise value of 17.65B yen. The company’s net tangible assets (NTA) total 15.4B yen, and its net current asset value (NCAV) stands at 13.48B yen, both significantly higher than the current market cap. These figures don’t account for the market value of the company’s properties, which are still undervalued on its books.

For the fiscal year ending May 31, 2025, Mitachi is forecasting an operating profit of 2.1B yen and a net profit of 1.6B yen, which translates to roughly 200 yen per share. In other words, Mitachi is trading at less than six times earnings. Assuming the company maintains its current payout ratio of 30%, shareholders could receive a dividend of 60 yen per share, which would yield 5.1% at current prices. (This is notably high given Japan’s low cash rates.) While earnings have fluctuated, Mitachi has remained consistently profitable, with only one unprofitable year since FY02. The company is increasingly exposed to the automotive sector, which could be affected by the impact of tariffs, particularly those from the Trump administration. While the near-term outlook remains uncertain, Mitachi appears to be a well-run business trading well below its liquidation value.

Finally, I had a large cash position due to some special situations (including CRGX) winding up. This helped reduce volatility in the portfolio during recent weeks due to Trump's tariffs announcements. This was not due to any special foresight on my part; I simply got lucky. My belief is that, at the size of my asset base, I should always be able to find things to do. Therefore, I should almost always be fully invested (or close to it). However, if I don't have things to do, experience has made me realise that it's OK to wait. I'll find opportunities eventually. At the moment, I have about 33% of the portfolio in cash, which is the highest level I can remember. I'm hoping I can find good ideas soon, but I'm still not finding extremely compelling valuations on my watchlist (at least for now).

As always, I like to talk to like-minded investors looking at similar things to me (namely net-nets, special situations and busted biotechs at the moment). If you’d like to get in touch, feel free to send me a message on Substack or a DM on Twitter.

HK listed China biotechs have gone from zero to hero in Q125. Check out 1672.hk and 9926.hk for example. Then there's 2696.hk that the major shareholder tried to privatize but got greedy and failed.

Recently did a round-up of biotech strategic reviews, though not a core focus (as reverse mergers seem too speculative), if that's useful: https://catalystbulletin.substack.com/p/biotech-strategic-reviews-round-up